Chips Rip, Software Splits, and Oil Slides on Diplomacy

Weekly Breakdown for the Week of May 4-8, 2026

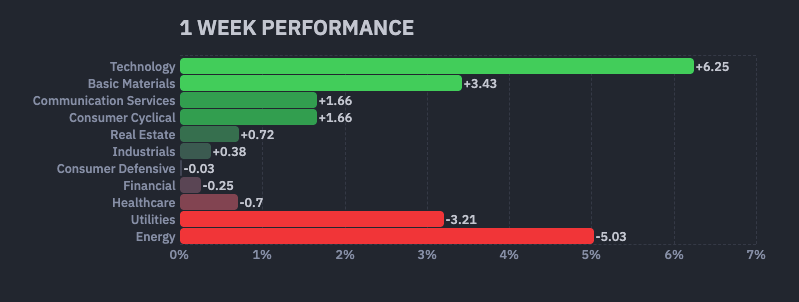

Tech Rally Diverges From the Rest of the Market

Markets posted a strong week, but the gains were anything but broad. The Nasdaq (QQQ) surged roughly 5.5% as the AI and semiconductor trade extended its run, while the S&P 500 (SPY) gained roughly 2.5% and the Dow (DIA) finished essentially flat. The Russell 2000 (IWM) added roughly 2%.

The split between the Nasdaq and the Dow tells the story of the week. Technology and communication services led, while energy fell sharply on a softer oil tape. The Tech Select SPDR (XLK) gained roughly 8% on the week, by far the biggest sector move, while the Energy Select SPDR (XLE) fell roughly 5%.

That dispersion came against a backdrop of mixed macro signals. The April jobs report came in well above expectations on Friday, but consumer sentiment hit a record low on the same day. The Iran war remains unresolved and the Strait of Hormuz remains closed, but oil fell on the week as nuclear deal negotiation rumors gained traction. CPI lands Tuesday and will be the next major test for the rally.

AMD Posts Blowout Q1, Data Center Segment Up 57%

AMD (AMD) reported Tuesday after the close, delivering an impressive quarter.

Revenue beat estimates, EPS came in well above the Street, and Data Center revenue grew 57% year-over-year, driven by strong demand for EPYC server CPUs and Instinct GPUs.

The stock jumped sharply on Wednesday and continued to grind higher throughout the week, finishing up roughly 26%, including an 11% rally on Friday alone.

A new partnership with Rackspace (RXT) was announced Friday, sending Rackspace shares more than 50% higher and adding another tailwind to the AMD story.

The market is now pricing AMD as a true peer of Nvidia (NVDA) in the AI compute race rather than a distant second. Some analysts have begun to question whether the valuation has gotten ahead of itself, but for now, the trend remains intact, and the data center growth numbers are difficult to argue with.

Intel’s Parabolic Run Draws Cisco Bubble Comparisons

Intel (INTC) gained roughly 25% on the week, capped by a 14% Friday rally that pushed the stock to a fresh year high. The catalyst this week was a combination of factors: continued enthusiasm around AI inference workloads favoring CPUs, ongoing speculation about an Apple-Intel manufacturing partnership, and the company’s sixth consecutive revenue beat from the prior earnings print.

The price action has now drawn comparisons to Cisco at the peak of the dot-com bubble. Intel currently trades at over 100x forward earnings and sits almost 200%above its 200-day moving average.

Several Wall Street analysts have started flagging valuation risk even while maintaining buy ratings.

Software Splits Along the AI Infrastructure Line

The software space broke into two cleanly separated camps this week. The iShares Software ETF (IGV) was up roughly 5% on the week, a strong showing that masked some of the dispersion of the earnings season.

The winners were the names that directly benefit from the AI infrastructure buildout.

Datadog (DDOG) gained a stunning 42% on the week after Thursday night’s earnings beat, with management raising guidance on the back of accelerating AI workload monitoring.

Akamai (AKAM) also rallied roughly 42% on a strong Q1 print as edge and CDN demand from AI inference workloads accelerated.

JFrog (FROG) jumped roughly 41% on its own beat, riding the same theme around devops infrastructure for AI deployment. Fortinet (FTNT) rallied roughly 32% on a clean cybersecurity beat.

Even names that didn’t report this week, like CrowdStrike (CRWD) and Palo Alto Networks (PANW), gained considerably as the AI infrastructure theme lifted everything in its path.

The losers told a very different story. Cloudflare (NET) beat on both EPS and revenue and even raised full-year guidance, but the stock fell roughly 24% on Friday and finished the week down roughly 10% after announcing a 20% workforce cut to pivot to an “agentic AI” operating model alongside softer near-term guidance.

HubSpot (HUBS) followed the same playbook with a weaker Q1 and Q2 guide and an AI-agent sales strategy pivot, falling roughly 18% on the week to a 52-week low.

The Trade Desk (TTD) missed badly on EPS ($0.08 versus a $0.32 estimate) and fell roughly 5%.

Palantir (PLTR) beat estimates but sold off roughly 4% as a strong pre-print rally faded

DXC Technology (DXC) was crushed for roughly 21% on Friday on disappointing earnings.

The market is paying a premium for software companies that sell into the AI buildout (monitoring, security, edge infrastructure, devops) while punishing companies whose pitch is “AI is replacing our headcount” or whose business model looks vulnerable to AI displacement.

Coinbase Misses Big as Bitcoin Reclaims $80K

Coinbase (COIN) reported Thursday after the close and posted a sharp earnings miss, with EPS coming in at –$1.49 versus expectations near breakeven. Revenue also came in below estimates.

The stock initially sold off but rallied roughly 4% on Friday alongside the broader risk-on tape, finishing the week up roughly 5%.

Bitcoin reclaimed the $80,000 level mid-week for the first time since January 2026.

Strong Jobs Report, Record-Low Consumer Sentiment

April nonfarm payrolls came in at 115,000 on Friday, well above the estimate. The unemployment rate held at 4.3%, and average hourly earnings rose 3.6% year-over-year.

The headline strength reinforced the Fed’s view that it can afford to hold rates steady while it waits for more clarity on inflation.

But the same morning brought a starkly different signal. The University of Michigan’s preliminary May consumer sentiment reading dropped to 48.2, a fresh record low, with current conditions falling to 47.8.

High gas prices and the ongoing war in Iran were the main drivers cited in the survey. Notably, one-year inflation expectations actually fell to 4.5% from 4.7%, but that was little comfort to a consumer base reporting the lowest sentiment readings on record.

The bifurcation between hard data and soft data continues to define the macro picture. Employers are still adding jobs, but consumers are increasingly anxious.

Markets are siding with the hard data for now.

Iran War Continues, Oil Falls on Diplomacy Hopes

WTI crude fell roughly 6% on the week to close near $95, despite the Strait of Hormuz still closed and the war in Iran ongoing.

The catalyst was reports of advancing US-Iran nuclear deal negotiations, which the market is pricing as the start of a path toward de-escalation.

Whether the optimism is justified remains an open question. Treasury markets are pricing in a more protracted conflict than equity markets are, with bond traders reluctant to fully embrace the diplomatic narrative. Energy stocks were the worst-performing sector of the week, with the Energy Select SPDR (XLE) down roughly 5%.

For traders, this remains a situation where headlines can move oil sharply in either direction on minimal notice. The next major catalyst is anything concrete out of the diplomacy track.

Sector Weekly Performance

Current Themes & Volatile Movers

Headline Reactions

MU up roughly 38% on the week, the stock’s best week in nearly two decades, on memory supply tightness and AI demand. Market cap surpassed JPMorgan.

SNDK up roughly 32% on the week as the memory complex went parabolic.

INTC up roughly 25% on the week as the AI inference rally and Apple manufacturing partnership rumors continued to fuel a parabolic run, capped by a 14% Friday rally.

QCOM up roughly 24% on the week, riding the broader chip momentum.

CRWD up roughly 16% on the week, lifted by the AI infrastructure software theme even without an earnings catalyst.

PANW up roughly 15% on the week on the same theme.

WDC up roughly 11% on the week.

SMH up roughly 11% on the week as semiconductors led the broader rally to a new high.

TWLO up roughly 10% on the week, riding the AI infrastructure software theme after its prior-week earnings beat.

TSLA up roughly 10% on the week.

NVDA up roughly 9% on the week to a new year high.

XLK up roughly 8% on the week, the strongest sector performer by a wide margin.

STX up roughly 8% on the week.

MSTR up roughly 6% on the week as Bitcoin pushed back above $80K.

AAPL up roughly 5% on the week to a new year high.

GOOGL up roughly 4% on the week to a new year high.

Earnings Reactions

DDOG up roughly 42% on the week after a Q1 beat and raised guidance tied to AI workload monitoring demand.

AKAM up roughly 42% on the week on a strong Q1 print as edge and CDN demand accelerated.

FROG up roughly 41% on the week after a Q1 beat as devops infrastructure benefited from AI deployment.

FTNT up roughly 32% on the week on a clean cybersecurity Q1 beat.

AMD up roughly 26% on the week, including 11% Friday, after a Q1 beat and 57% YoY Data Center revenue growth.

OSCR up roughly 15% on the week after a massive Q1 beat ($2.07 EPS versus $1.11 estimate).

BILL up roughly 7% on the week on a Q1 beat.

COIN up roughly 5% on the week despite a sharp Q1 EPS miss, helped by a Friday rally on the jobs print.

XYZ up roughly 4% on the week after Block’s Q1 beat.

PLTR down roughly 4% on the week despite a Q1 beat as a strong pre-print rally faded.

MCD down roughly 4% on the week despite a Q1 beat.

TTD down roughly 5% on the week after a sharp EPS miss ($0.08 versus $0.32 estimate).

VST down roughly 5% on the week despite a Q1 beat.

DASH down roughly 7% on the week after missing on revenue.

RBLX down roughly 7% on the week, continuing to slide after the prior week’s earnings.

NET down roughly 10% on the week including a 24% Friday drop, after announcing a 20% workforce cut and softer near-term guidance despite a Q1 beat.

MELI down roughly 12% on the week after a Q1 EPS miss.

SHOP down roughly 14% on the week despite a Q1 beat as forward guidance disappointed.

HUBS down roughly 18% on the week including a 19% Friday drop, finishing at a 52-week low after weak Q1 and Q2 revenue guidance and an AI-agent strategy pivot.

ANET down roughly 18% on the week despite a Q1 beat with revenue up 35% YoY, as elevated memory costs raised margin concerns.

WHR down roughly 21% on the week after a sharp Q1 EPS miss.

RXT up roughly 210% on the week, including a 56% Friday gain, after announcing a multiyear AI infrastructure partnership with AMD and reporting Q1 earnings Thursday morning.

FLNC up roughly 98% on the week after a Q1 EPS beat Wednesday night, with shares ripping as the AI data center power story extended into battery storage names.

INOD up roughly 93% on the week after a massive Q1 beat ($0.42 EPS versus $0.13 estimate, revenue up 54% YoY) and raised 2026 guidance tied to AI data services demand.

RKLB up roughly 34% on the week to a fresh all-time high after a Q1 revenue beat and the announcement of the largest launch contract in the company’s history.

DXC down roughly 21% Friday on disappointing earnings.

Market & Economic News

April nonfarm payrolls came in at 115,000, well above the 62,000 estimate, with the unemployment rate steady at 4.3%.

University of Michigan May consumer sentiment fell to a record low of 48.2.

WTI crude closed near $95 per barrel, down roughly 6% on the week, despite the Strait of Hormuz remaining closed.

US-Iran nuclear deal negotiations were widely cited as the catalyst behind oil’s decline.

Bitcoin traded above $80,000 for the first time in months, reaching roughly $81,400 mid-week before settling near $80,100.

Gold gained roughly 2% on the week to close near $4,730 per ounce.

The Treasury market continued to price in a more protracted Iran conflict than the equity market, leading to divergent risk signals.

President Trump delayed new EU tariffs to July 4.

Challenger Job Cuts surged to roughly 83,000 in April, with tech sector layoffs accelerating.

CPI lands Tuesday and is expected to be the next major catalyst, with consensus calling for headline inflation to tick higher.

Upcoming Earnings

Monday 5/11/26

CRCL, CEG, B, MNDY, MOS, CGBD, CRON, FSK, VFF, HIMS, ASTS, PLUG, RGTI, MARA, BW, ACHR, CLSK, GPRO, MVST

Tuesday 5/12/26

QBTS, AG, KOPN, VG, ONON, SE, JD, ACHV, BETA, AMTM, OKLO, KRMN, ELMD, NXT, FNV, AEYE, ANDG, ATRO, OPRX, EVLV

Wednesday 5/13/26

NBIS, BABA, EOSE, DT, WIX, ICL, VLN, VSH, GLBE, ENVX, CSCO, USAR, AQST, DOCS, CPA, LESL, FLNT

Thursday 5/14/26

ONDS, BN, KLAR, LUNR, BLSH, IMSR, SBC, BRFH, SUNS, VIK, NU, FIG, AMAT, NN, RUM, BZAI, BLNE, YETI, CODX, BSEM

Friday 5/15/26

SPRY, HTHT, PAVM, RMIX, SACH, SLE, AZ, ALK, MHH, RBC

Upcoming Economic Events & Data

Monday 5/11/26

Existing Home Sales (Apr)

CB Employment Trends Index (Apr)

3-Year Note Auction

3-Month and 6-Month Bill Auctions

Tuesday 5/12/26

CPI MoM (Apr)

CPI YoY (Apr)

Core CPI MoM (Apr)

Core CPI YoY (Apr)

NFIB Business Optimism Index (Apr)

Fed Williams Speech

Monthly Budget Statement (Apr)

10-Year Note Auction

Wednesday 5/13/26

PPI MoM (Apr)

Core PPI MoM (Apr)

PPI YoY (Apr)

MBA Mortgage Applications

EIA Crude Oil Stocks Change

OPEC Monthly Report

30-Year Bond Auction

Fed Kashkari Speech

Thursday 5/14/26

Retail Sales MoM (Apr)

Retail Sales Ex Autos MoM (Apr)

Initial Jobless Claims

Continuing Jobless Claims

Import Prices MoM (Apr)

Export Prices MoM (Apr)

Business Inventories MoM (Mar)

Fed Williams Speech

Friday 5/15/26

NY Empire State Manufacturing Index (May)

Industrial Production MoM (Apr)

Manufacturing Production MoM (Apr)

Capacity Utilization (Apr)

Baker Hughes Oil Rig Count